Rent Growth Lags for Efficiency Units

The multifamily industry continues to be in a period of considerable change. The effects of the new dynamics introduced in 2020 continue to ripple across the industry as it continues to move slowly but steadily toward normalization. In such periods, it is of particular importance to pay attention not just to market-level metrics, but also to the ever-changing situation below the market level. One such perspective is rent performance by floorplan type.

All numbers will refer to conventional properties of at least 50 units.

Efficiency Units

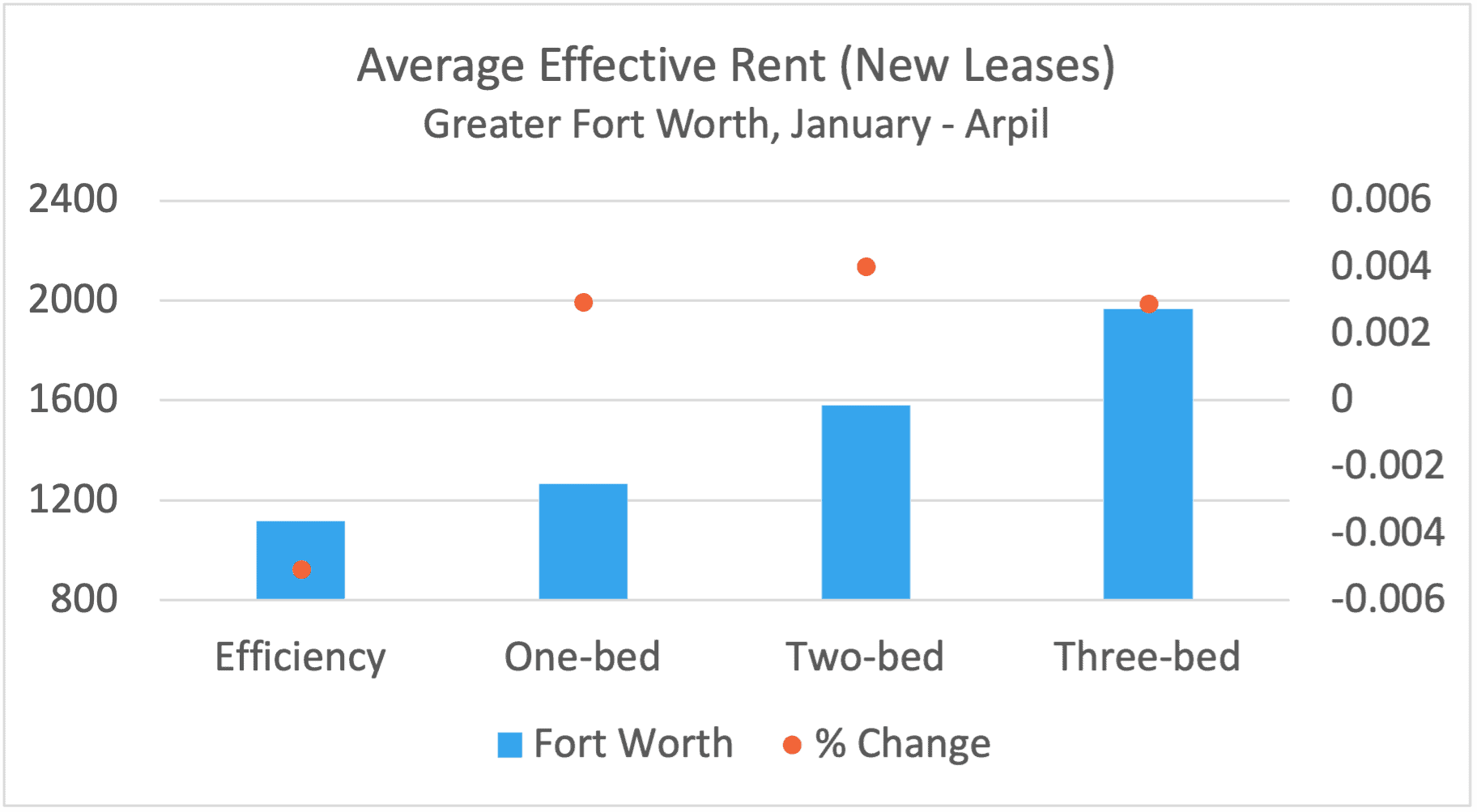

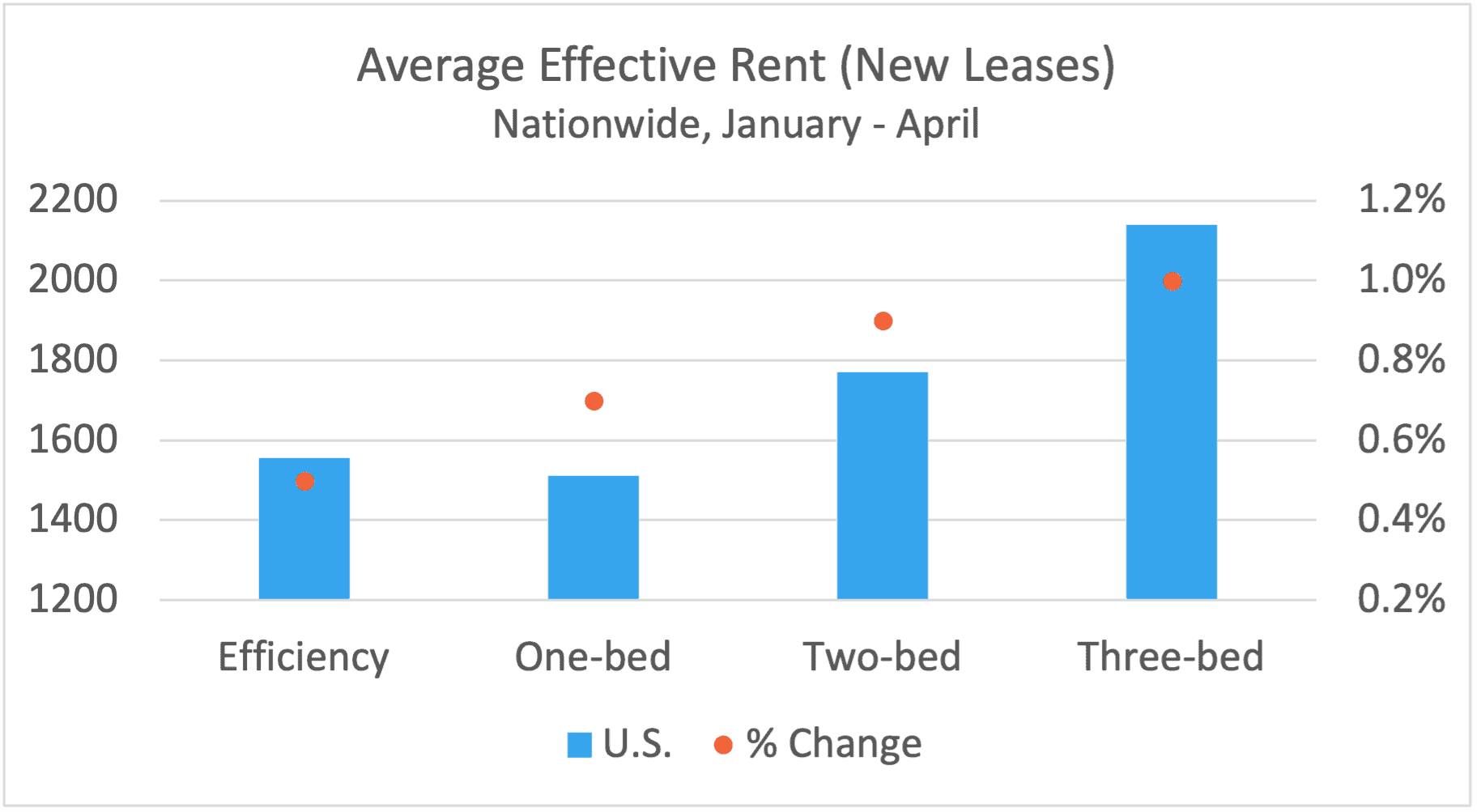

The most notable difference between Greater Fort Worth rent change and the nation for any floorplan has been in the efficiency units. This year through April, these units have seen average effective rent for new leases decline by 0.5%. The average unit ended April leasing for $1,117 for new residents. The efficiency subset was the only floorplan type to suffer a decline in the period, and no floorplan did the same at the national level. The decline at the average, although small, was the first decrease for this portion of the calendar of the last five years.

For lease concessions, the availability, and the average value both rose from the start of the year. Just less than 25% of efficiency units were offering a discount for new residents at the end of April – up nearly 40% from the start of 2023. The average discount value finished the period at a little above 7% of an annual lease. Stated another way, the average discount was a little under four weeks off of a twelve-month lease.

One and Two-bedroom Units

A 0.3% average effective rent increase through April for one-bedroom units across Greater Fort Worth was typical for the market to start the year outside of the efficiencies. The average one-bedroom unit closed April leasing for $1,265 per month after crossing $1,000 for the first time in the opening months of 2021.

However, the availability of lease concession rose more within the one-bedroom group than any other. An increase of a little more than 50% in the first four months of the year brought the availability of discounts for new residents to about 20% of units. This was well above last year’s trough in availability of below 10%, and well below the peak from the pandemic period, but not far from the pre-pandemic 2019 level.

Two-bedroom units have performed very similarly to the one-bedrooms to start the year. An average effective rent gain of 0.4% was slightly better but was even more muted in relation to previous years than was the case for the gain for one-bedrooms. The average unit ended April leasing for $1,582 per month after an increase in the period of less than $10.

Lease concession availability did not increase to quite the same magnitude as for the one-bedroom group, but nevertheless climbed by more than 40%. By the end of the period, roughly 20% of two-bedroom units were offering a lease concession for new residents. As was the case for every floorplan type, the rate of discount availability at the end of April was between the peaks and valleys of the 2020 through 2022 periods but not far from the 2019 level. An average lease concession value of just more than 5% off an annual lease edged out the one-bedroom subset for the lowest of any floorplan type.

Three-Bedroom Units

A 0.3% gain in average effective rent for three-bedroom units matched the change from the one-bedrooms and brought the average unit to $1,968 per month for a new resident. In recent years, with the exception of 2021, rent growth through April for three-bedroom units tended to be lower than for other floorplan types. This year, by matching the one-bedroom gain and beating the efficiency unit performance, 2023 can be added to the exceptions list.

The increase in lease concession availability for these units was the smallest of the floorplan groups. An increase of a bit under 30% meant that only around 17% of three-bedroom units were offering a discount for new leases at the end of April. This was not only the lowest availability rate of any floorplan but also made three-bedroom units the only group to end the period with lease concession availability lower than at the same point in 2019.

Takeaways

The Greater Fort Worth market has suffered a net loss in leased units in the opening four months of 2023. Although the margin was small at around 200 net units lost, this year was the first in more than a decade to see net absorption in negative territory this late in the calendar year.

Average effective rent growth, while slightly positive at the market level, has similarly been more tepid so far this year than in any year of the last ten. Efficiency units represented a particular problem area with a decline in the period, but no floorplan type managed a gain of even fifty basis points through April. To be sure, in some markets around the country the picture is darker. And yet, the widespread nature of tepid rent growth has provided a reminder that aside from 2020, gains will be much harder to come by in 2023 than has been the case this side of the Great recession.

Jordan Brooks

Senior Market Analyst – ALN Apartment Data

Jordan@alndata.com

www.alndata.com

Jordan Brooks is a Senior Market Analyst at ALN Apartment Data. In addition to speaking at affiliates around the country, Jordan writes ALN’s monthly newsletter analyzing various aspects of industry performance and contributes monthly to multiple multifamily publications. He earned a master’s degree from the University of Texas at Dallas in Business Analytics.